{kind=link}

User-first reality

Most people need cash fast. They want clarity and low friction. This guide shows precise moves to get the best from instant loans and how DiDi’s product fits. Start by checking didi prestamos for the baseline offer and eligibility rules. Expect short approval windows, clear APRs, and simple digital onboarding.

What matters to you — and why

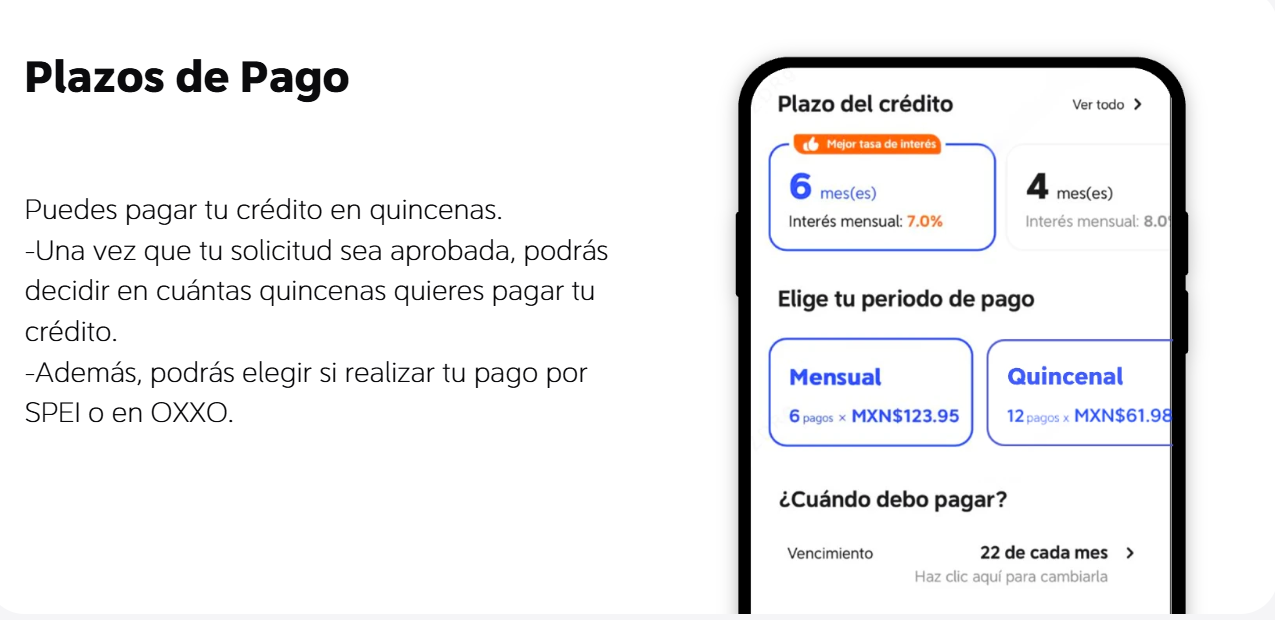

Focus on three user priorities: speed, cost, and predictability. Speed means quick verification and fast disbursement. Cost is APR, fees, and any origination charges. Predictability covers fixed loan terms and clear repayment dates. Measure each offer against those criteria before committing.

Step-by-step to maximize benefit

Follow this tight checklist to improve outcomes:

– Confirm required documents and have them ready (ID, bank link, proof of income).

– Pre-check your credit score and remove simple errors that lower it.

– Compare APR and total repayment, not only monthly payment.

– Choose the shortest loan term you can afford to reduce interest paid.

– Use digital wallets or direct deposit to avoid transfer delays.

These moves cut cost and time. A lean stack of paperwork speeds underwriting and funding.

Common mistakes to avoid

People default to the fastest disbursement without checking effective cost. They ignore origination fees or variable rates. Others stretch the loan term to lower monthly payments, then pay far more interest. Avoid auto-renewals and skip duplicate applications — those harm your credit score and slow approval.

How DiDi Finanzas fits in practice

DiDi Finanzas is built for drivers and urban users who need rapid access. After the 2020 COVID-19 period in Mexico City, demand for quick online credit rose sharply — firms optimized for speed and lower friction. DiDi’s flow aims to match that demand: straightforward digital KYC, clear APR displays, and faster payout windows than many traditional lenders.

When to pick DiDi and when to look elsewhere

Pick DiDi if you need near-instant funding, a simple app experience, and transparent fees. Look elsewhere for large, long-term loans or when you need complex refinancing. Alternatives include banks (better for long-term rates) and credit unions (may have lower fees but slower processes). Balance choice with need: convenience vs. lowest lifetime cost.

Practical tips from users and data

Users who prepare docs and check score first get approved faster. Keep payment reminders and link a primary account for debit. Use electronic statements to meet verification. Industry terms to know: credit score, APR, loan term. Small actions lower default risk — lenders then offer better repeat rates.

Quick checklist before you accept

– Confirm total repayment amount, not just monthly.

– Check for prepayment penalties.

– Verify fund delivery time and method.

– Read fine print on auto-renewal and late fees.

Golden rules for decision-makers

Three metrics to drive selection:

1) True cost: compute total interest plus fees over the loan term. Use that as the first filter.

2) Time to funds: measure onboarding to disbursement in hours, not days.

3) Flexibility: look for one-time prepay without penalty and a realistic repayment calendar.

Wrap and value

Follow the checklist and metrics. Prepare documentation, compare APR and total cost, and favor shorter terms when feasible. These steps reduce cost and speed access.

DiDi Finanzas often sits where speed and clarity matter most — a practical solution for instant needs and predictable terms. –